What You Don’t Know Could Hurt You

Uncovering Gaps In Your Malpractice Policy

As a healthcare provider, you have a flurry of coverages available to you – all designed to protect your livelihood. So how do you decide what coverages matters most? Arguably the most critical coverage decision is selecting a quality malpractice policy. Your malpractice policy is designed to defend your professional decisions, reputation and even your license to practice. While coverage options may be very close in cost, they may differ widely in coverage. Do you know the differences?

Procedural Exclusions and Carve Outs

Many healthcare providers consider malpractice insurance to be a commodity and prioritize pricing and customer service over coverage. Even though there are a fair amount of similarities, missing one key coverage could put you at substantial risk.

For example, a doctor who was doing pain management procedures wanted to cancel his policy since he was being added to another doctor’s policy. The new policy had an endorsement excluding coverage for spinal injections and platelet rich injections. However, the doctor performed both of these procedures thereby causing a potential gap in coverage.

Another healthcare provider needed coverage for patient care he was providing at a correctional facility. He purchased a new policy to ensure he had the appropriate coverage. Unfortunately, he hadn’t noticed that the new policy specifically excluded one of the services that he was expected it to provide. It is critical to thoroughly review the coverage if you purchase it directly from the insurance carrier.

Lastly, an owner of a counseling clinic requested a review of the clinic’s current insurance agreement. The clinic did medication management, and the nurse practitioners were responsible for prescribing medication to patients. Unfortunately, their insurance policy specifically excluded coverage unless medications were prescribed by a physician. Even though the nurse practitioners had their own policy, they would not have had coverage if the clinic was sued.

License Complaints

Most policies provide coverage if you’re brought before a licensing board to respond to a complaint. One difference is whether they provide an attorney or whether you need to hire an attorney first and ask the insurance carrier to reimburse you for your incurred expenses.

Who is covered by Your Policy?

Physicians, CRNAs, nurse midwives, and chiropractors will need to be listed by name on the policy (scheduled), but other classes of healthcare providers will have automatic coverage. Always review your new policy carefully when you change insurance companies. If the new policy requires specific providers be listed and they aren’t, your claim could be declined.

Extended Reporting (Tail) Endorsement

This coverage will back you up when you close/sell or leave the business.

- Unlimited – provides indefinite coverage and limits reinstate for a certain number of years. The rates are filed with the state and typically are around 150 to 200% of your current premium.

- Limited – the limits don’t reinstate and the coverage lasts for a set time (usually five years). The premium is shown in the declarations page.

- Very Limited – the coverage is limited to a couple of years and the premium is determined at the time of the cancellation.

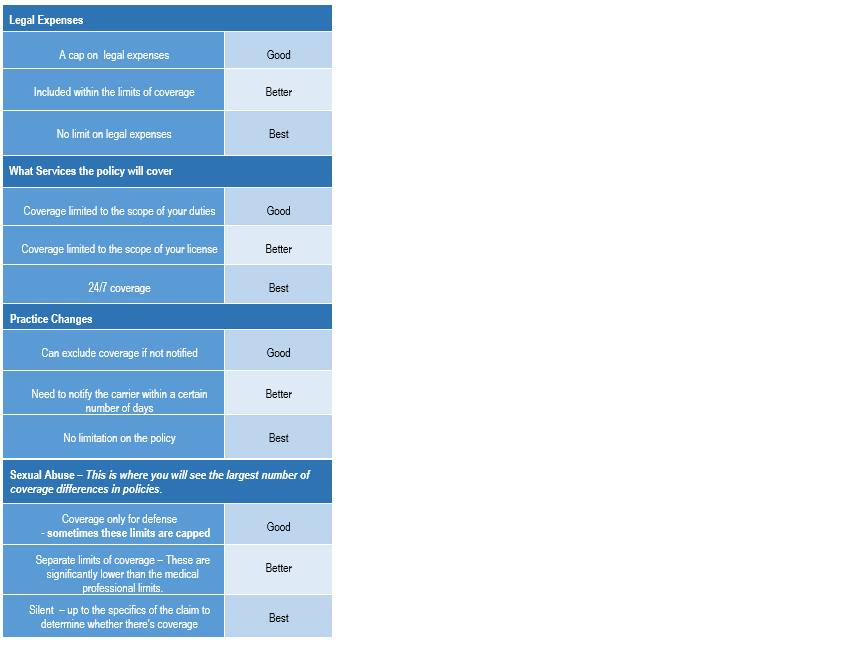

Good, Better or Best – Evaluating Your Risk Tolerance

When selecting coverage, you will need to consider your risk tolerance related to the following coverage components. What protection level is important to you – good, better or best?

Other Key Considerations

Do you know if you have the final say on when the claim is considered settled? There are two types of Consent to Settle coverage options that impact who determines when the claim is settled.

- Full Consent to Settle: this is when the insured has the final say on when a claim is settled, and

- Consent to Settle with a hammer clause: The insured does have the final say but if there’s a verdict for the plaintiff, the insured will share in the loss.

And finally, you will need to determine what type of event will force the policy to respond, also known as the Coverage Trigger. Coverage could be an incident trigger. For example, if a patient passed away, the policy would respond when you, as the healthcare provider, report the incident to your insurance carrier. Or you could have a written damages trigger. In the same example, the policy wouldn’t respond until the patient’s family requests to be reimbursed for damages.

If you move from a written damages to an incident policy while there is an impending patient death suit but before you have received the written demand, the malpractice carrier may decline coverage because they weren’t adequately notified.

COVID-19 Virus Exclusions

Due to COVID, you should be on the lookout for virus exclusions. They are already happening on non-standard policies but expect this to trickle down to standard lines carriers as well.

If you have questions about your medical malpractice coverage or other insurance policies, please Dyste Williams.

LEAVE A COMMENT